(8 min read)

It doesn’t matter if you hear it from a doctor, a teacher, or a financial regulator, the word “exam” is rarely something to look forward to. Whatever the topic, it means some part of you, your work, or your business is about to face careful scrutiny.

Exams are a fact of life in financial services, but preparation can reduce much of the pain. When regulators come calling, it’s best to have a good sense of what they’ll want to look at and how you plan to respond.

Exams Are All About Risk

Financial regulations exist, by and large, to reign-in risk, as it relates to investors, issuers, market stability/fairness, and other stakeholders. It’s no wonder, then, that a regulatory exam from FINRA, the SEC, or some other industry watchdog, tends to focus on risk.

Broadly speaking, regulators usually want to know how your firm takes risks, where your firm allocates risks, and whether your firm creates risks.

In other words, are you acting as an honest broker, a careful fiduciary, and a responsible market participant?

Of course, your response to those questions is “yes, yes, and yes,” so how can you anticipate where regulators will, specifically, focus their attention?

Here are some reliable indicators:

How You Make Most of Your Money

An examiner is likely to want to explore the most lucrative practice or product line in your business. This is just old hat for regulators.

Outsized revenue (or losses) can signal outsized risk-taking with client money.

Similarly, if you have a high-volume line of business generating a disproportionate share of revenue, regardless of the risk to which it puts individual clients, you can be sure regulators will want to take a look at it.

Lax record-keeping and other risky, corner-cutting practices can many times make regular bedfellows with high-volume business lines.

So, take extra time now to make sure everything is ship-shape as it relates to these.

Trending Topics

Hot topics in financial regulation follow cycles roughly correlated to social and political trends.

Regulatory priorities evolve with changes in administrations, market developments and crises, and even individual regulators’ personal agendas. There’s no reason for your firm to get blindsided by changing priorities, however.

Most regulators give clear signals of where they expect to focus their attention in exams, both through messaging from regulatory leaders in speeches and op-eds, and directly through advisories posted to their websites.

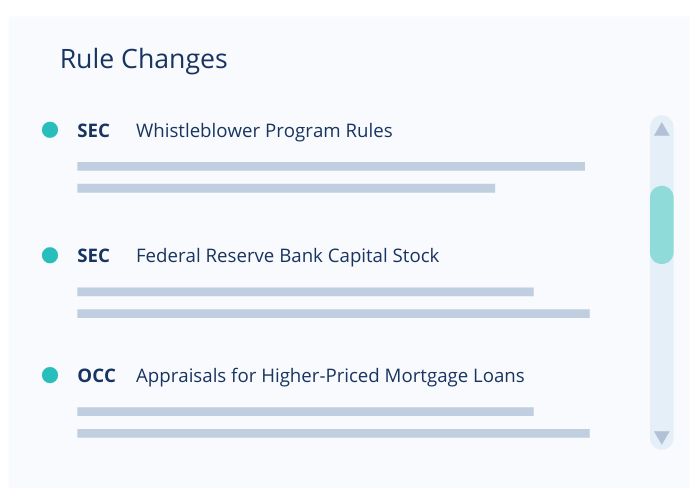

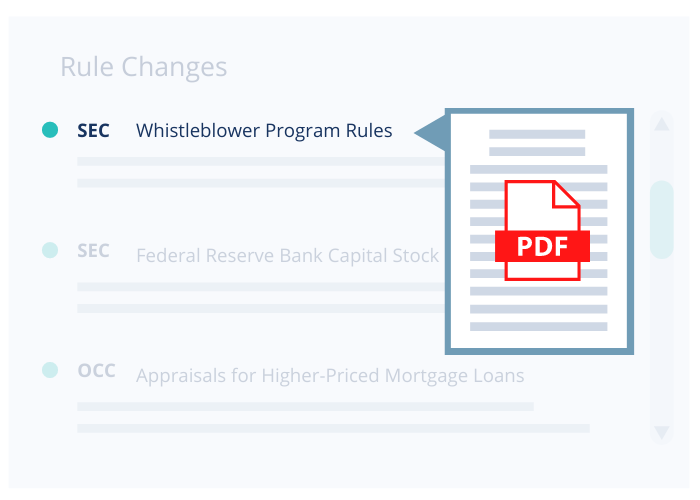

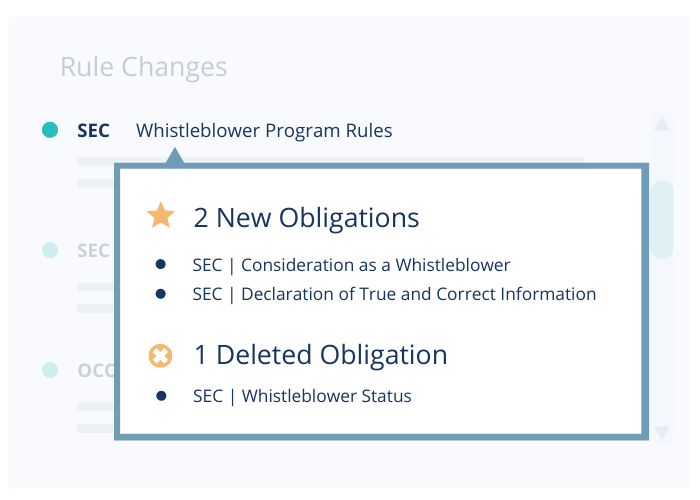

For example, here are the 2019 exam priorities published by FINRA and the SEC. Read them and come up with a proactive game plan for how your firm will address each hot-button topic area.

Prior Period Challenges

If your firm faced regulatory discipline in prior periods, then you can be confident a regulatory exam will revisit the same areas to see if the previous deficiencies have been fixed, which you’d think is common sense, but you’d be surprised how many times this can slip through the cracks. Regulators want to rule out the possibility that past violations reflect an endemic flaw in your business practices.

They do so by looking for evidence that you’ve taken appropriate steps to avoid similar violations.

Make a regular, periodic practice now of reviewing old violations, remedial measures you took at the time, and where those efforts stand today.

You can gain significant credibility with examiners by speaking fluently and confidently about past violations, lessons learned, and firm-wide improvements.

In many cases, even though it may be tough to swallow your pride, thanking your examiners for identifying the previous violations and stating that it was able to help you strengthen your compliance program may even help you build rapport and give you ethical credibility with them.

Conversely, you will lose credibility if you (even inadvertently) signal to examiners you consider past discipline to have been unwarranted, they are “no big deal”, or that you blatantly disagree with them (so make sure not to do this!).

Anything That Escaped Scrutiny Last Time and Has Changed

Reflect back on your last regulatory exam and identify the practices or business lines that did not get attention or did not exist back then.

As a rule of thumb, if any of those practices or lines have changed significantly in the interim in terms of their revenue generation or risk profile, then examiners will likely want to look at them.

This applies to business shifts in either “direction”; i.e., take an objective look at facets of your business that materially succeeded, as well as those that woefully failed, since your last exam.

Be prepared to explain those shifts, including any significant costs that drove you away from a practice or line, any efficiencies or opportunities that attracted you to another, and (most importantly) any regulatory issues you recognized and addressed involving them.

Explore Enforcement and Rulemaking Efforts

Sometimes the enforcement efforts and rulemakings a regulator engages in speak even louder than annual regulatory guidance on exam priorities.

Stay current on peers who have been named in disciplinary actions by your examining regulator, and read carefully as to why, as if you have a similarly deficient process, it may be your chance to be ahead of the curve and fix the problem before the regulators arrive.

This can be done by reading press releases and enforcement filings on regulators’ websites (Ascent curates a proprietary library of these types of documents, across all regulators for you automatically, which helps save time rather than scouring through several regulatory websites).

Likewise, treat rulemakings as a leading indicator of what regulators will start caring about next.

Anticipated future rules may even influence examiners in deciding what to dig into on a visit to your firm, so be sure to stay on top of these as well.

If you are like most other compliance officers, you probably don’t have a ton of time to set aside to read a whole proposed rule.

Ascent’s targeted delivery of rule updates, tailored to your business in real-time, can help focus you in on the potential areas of examiners’ interest that apply to the business you transact, saving you tons of time on both the front and back ends.

Face Exams with Confidence

Ascent streamlines regulatory compliance by giving financial services firms clear and timely visibility into their specific regulatory obligations.

Our powerful Regulation AI maps regulatory text to your specific business, offering you real-time insight into the steps you need to take to stay in compliance, as well as an audit trail of every activity completed so you can easily show evidence of your end-to-end compliance.

With Ascent’s help, you can feel confident when your exams come around, knowing you’ve taken the appropriate steps to keep your business violation-free.

Enjoy this article? Subscribe to receive helpful content designed to help you win at compliance.

Subscribe